Imagine you're looking at two different savings accounts. One offers a 1% interest rate, and the other offers 4%. It's instantly obvious which one will earn you more money.

The capitalization rate, or cap rate, does a similar thing for real estate investments. It’s a helpful metric that shows you a property's potential annual return before you factor in financing. Even if you're buying a primary home, understanding the cap rate can give you a peek into its future investment potential, should you ever decide to rent it out.

Decoding Capitalization Rate

When you start your home-buying journey, you'll hear a lot of new jargon. While the cap rate is mostly used by investors, it's a useful concept for any buyer to understand. Why? Because it offers a clear, simple way to evaluate a property's income-producing potential.

Think of it as the property's financial pulse.

In simple terms, the cap rate measures the relationship between a property’s annual income (its Net Operating Income, or NOI) and its current market value. It answers a fundamental question: "If this property were a rental, how much income would it generate each year relative to its price?"

A cap rate is a simple way to show how much income a property produces relative to its price. A 5% cap rate means the property generates 5 cents in annual income for every $1.00 of its market value.

This single percentage is a handy tool. It lets you quickly compare the income potential of different properties—a duplex in one neighborhood versus a condo across town—on an apples-to-apples basis, no matter their size or price tag.

To give you a quick reference, here’s a simple breakdown of what goes into a cap rate calculation.

Cap Rate at a Glance

| Component | What It Means | Why It Matters for a Buyer |

|---|---|---|

| Net Operating Income (NOI) | The property's total potential rental income minus its operating expenses (before loan payments). | This shows the pure profit the property could generate on its own. |

| Property Value/Price | The current market value or the price you'd pay for the home. | This is your initial investment, the foundation of the calculation. |

| The Cap Rate % | The resulting percentage (NOI ÷ Value). | It represents the unleveraged annual rate of return on the property as a rental. |

This table shows how these simple inputs come together to create a powerful metric for understanding a property's financial health.

Why It Matters to You

Getting a basic handle on cap rates can help you make a smarter buying decision, even if you don't plan to be a landlord right away. Here's why:

- Future-Proofing Your Purchase: Your first home might become a rental property down the road. Knowing its potential cap rate gives you insight into its long-term value as an asset.

- Understanding Market Value: In areas with a lot of rental properties, cap rates influence home prices. A property with strong income potential is often valued higher.

- Spotting a Good Deal: A property with a healthy potential cap rate might be a sign of a well-priced home in an area with strong rental demand, which is often a good indicator of a stable neighborhood.

The cap rate is a fundamental metric used by investors to value income-producing real estate. For a more technical breakdown, this detailed guide on What is Cap Rate in Real Estate for Investors is a great resource. While they fluctuate with the market, cap rates have historically hovered in the 8% to 12% range for many commercial properties, giving investors a solid benchmark for what a "good" return looks like.

How To Calculate Cap Rate: A Real-World Example

Alright, enough with the theory. Let's walk through how to calculate a cap rate. You'll be surprised at how straightforward it is. The whole thing boils down to one simple formula, and working through an example is the best way to understand it.

The formula you need to remember is: Cap Rate = Net Operating Income (NOI) ÷ Property Value.

Let's break that down into a few simple, actionable steps.

Step 1: Find The Net Operating Income (NOI)

First, you need the property's Net Operating Income (NOI). Think of NOI as the property's potential annual profit from rent before you account for any loan payments. It's the money left over after you've collected all the income and paid all the bills required to keep the property running.

Getting to your NOI is a two-part process:

- Figure Out the Gross Annual Income: Add up every dollar the property could bring in over a year. This is mostly rent, but you can also include other income streams like fees for parking or laundry. To find this for a home you want to buy, you can look up average rents for similar properties in the area.

- Subtract Annual Operating Expenses: Now, subtract all the costs of running the place. We're talking about property taxes, insurance, property management fees (even if you plan to self-manage, it's good to include a fee for your time), routine maintenance, and repairs.

Crucial Note: Your mortgage payment (the principal and interest) is never included when calculating NOI. The cap rate is designed to measure a property's raw performance, independent of how you finance it. This lets you make a true apples-to-apples comparison between properties.

Step 2: Determine The Property's Value

This part is usually pretty simple. If you're looking to buy a home, the "value" is the asking price or what you expect to pay for it.

If you already own the property and want to know its current cap rate, you'd use its current market value. You could get this from a recent appraisal or by asking a real estate agent for a comparative market analysis (CMA).

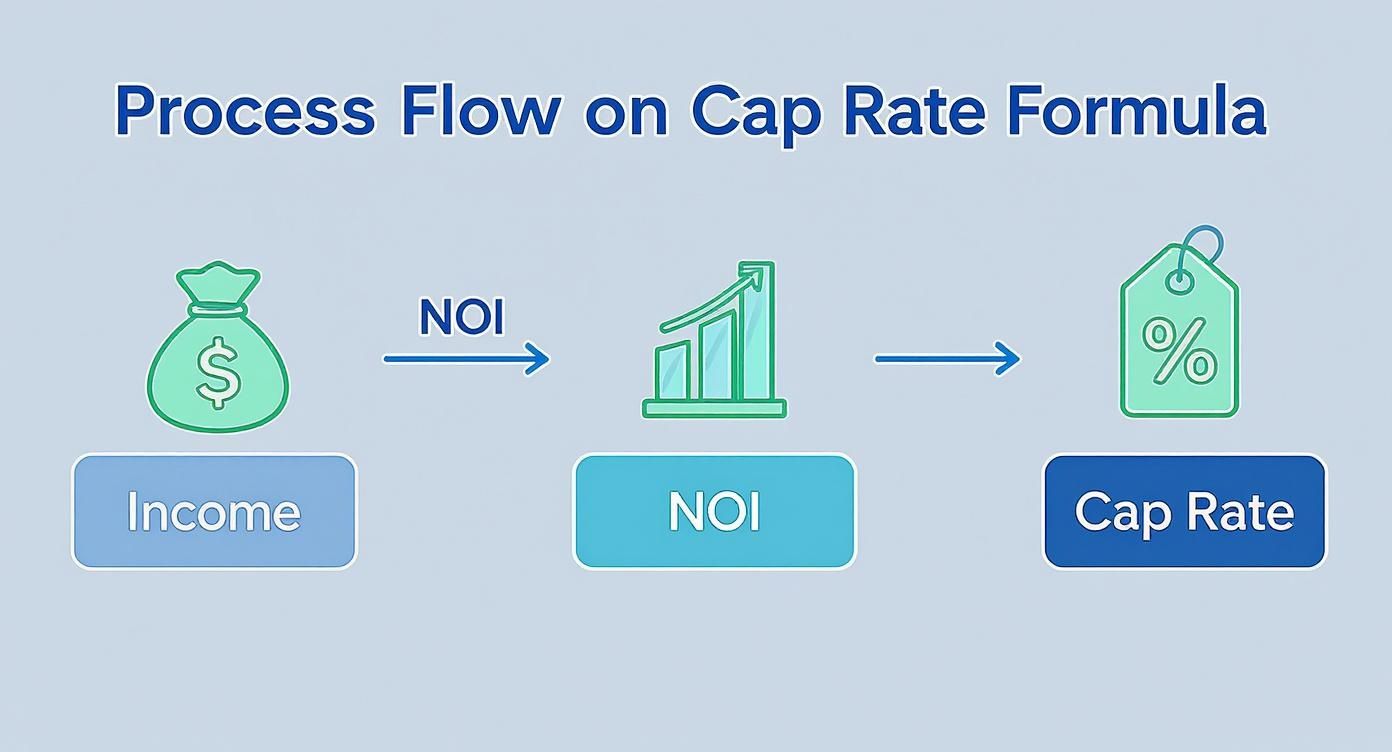

This flow chart gives you a great visual of how income and expenses are distilled down into the final cap rate percentage.

As you can see, you take all the income, subtract all the operating costs to get your NOI, and then divide that by the property's value. Simple as that.

A Worked Example: A Duplex Property

Let's run the numbers on a real-world scenario. Say you're analyzing a duplex with a list price of $400,000.

Income Calculation:

- Unit 1 Rent: $1,500/month

- Unit 2 Rent: $1,500/month

- Total Monthly Income: $3,000

- Gross Annual Income: $3,000 x 12 = $36,000

(For a much deeper dive on this, check out our full guide on how to calculate rental income properly.)

Expense Calculation:

- Property Taxes: $4,500/year

- Insurance: $1,200/year

- Vacancy (we'll estimate 5% of gross income): $1,800/year

- Repairs & Maintenance (a solid 8% estimate): $2,880/year

- Property Management (standard 10% fee): $3,600/year

- Total Annual Expenses:$13,980

Putting It All Together:

- Net Operating Income (NOI): $36,000 (Income) - $13,980 (Expenses) = $22,020

- Property Value:$400,000

Now, we just plug those numbers into our formula:

Cap Rate = $22,020 (NOI) ÷ $400,000 (Value) = 0.055

To turn that decimal into the percentage we always use for cap rates, just multiply by 100. For a quick primer on the math, this guide on understanding percentages is helpful.

The cap rate for this duplex is 5.5%. This is the key metric you'll use to compare this deal against any other investment property on your radar.

What a Good Cap Rate Actually Looks Like

So you’ve run the numbers and have a cap rate. Great. Now what? You’ve got a single percentage staring back at you, but what does that number actually mean? It’s tempting to search for a magical "good" cap rate, but the truth is, there isn't one.

A good cap rate is all about context. It’s a snapshot of the relationship between risk and reward for a specific property, in a specific market, at a specific time.

Think of it this way: a high cap rate is like a high-yield bond—it promises strong returns right away, but it often comes with more risk. A low cap rate is more like a blue-chip stock—the immediate returns might be smaller, but you’re banking on stability and long-term growth.

The High Risk, High Reward Scenario

Seeing a high cap rate, like 8% or 9%, can get an investor’s heart pumping. It signals strong cash flow. For example, a property priced at $200,000 with a 9% cap rate is generating $18,000 in Net Operating Income (NOI) a year. On paper, that’s a fantastic return.

But that high number always tells a story. A higher cap rate often hints at underlying issues:

- Higher Risk: The property might be in a less desirable neighborhood with unpredictable rental demand.

- Deferred Maintenance: That great cash flow could disappear fast if the building needs a new roof or HVAC system.

- Management Headaches: It could be an older property that demands constant attention and repairs.

For a home buyer, this could mean purchasing a home in an area with lower appreciation potential or facing unexpected repair bills.

The Low Risk, Steady Growth Scenario

On the other side of the coin, you have low cap rates, maybe around 4% or 5%. This is your classic low-risk, high-demand property. Picture a well-maintained home in a great school district or a condo in a booming downtown area.

A low cap rate usually means buyers and investors are willing to pay a premium for safety and stability. They expect less immediate cash flow but are betting on strong, reliable appreciation in property value over time.

While the day-one rental returns won't blow you away, these properties offer peace of mind. They’re generally in desirable locations, attract high-quality tenants if rented, and tend to hold their value better during economic downturns. It’s a different game entirely, which is why our complete guide on using the cap rate on a rental property is a must-read for investors trying to find the right balance.

To give you some real-world context, cap rates move with the economy. In the early 2000s, prime commercial properties in cities like New York often traded at 4% to 6% cap rates. After the 2008 crash, those same properties saw rates jump to 7%-10% as perceived risk shot through the roof. You can find more historical data like this over at Origin Investments.

High Cap Rate vs Low Cap Rate

To make it crystal clear, let's break down what high and low cap rates usually signal about a potential home purchase. This table gives you a side-by-side look at the trade-offs.

| Characteristic | High Cap Rate (e.g., 9%) | Low Cap Rate (e.g., 4%) |

|---|---|---|

| Potential Return | Higher immediate cash flow if rented | Lower immediate cash flow, higher appreciation potential |

| Perceived Risk | Higher (location, property condition) | Lower (stable location, good condition) |

| Property Class | Typically in developing or less sought-after areas | Typically in prime locations with high demand |

| Management Need | High-intensity if rented, may need more repairs | Lower-intensity, often move-in ready |

| Market Demand | Lower buyer demand, less competition | High buyer demand, very competitive |

| Growth Outlook | Potential income-focused if rented | Appreciation-focused, strong long-term value |

Ultimately, neither a high nor a low cap rate is inherently "good" or "bad." The right one for you depends entirely on your financial goals, risk tolerance, and what you're looking for in a home.

Using Cap Rate to Compare Investment Properties

This is where the cap rate becomes a powerful tool. It’s great for making true apples-to-apples comparisons, cutting through the noise of varying property prices, sizes, and potential rental incomes.

Imagine you're trying to choose between three completely different properties. How do you quickly and objectively figure out which one offers the most income potential for your money? The cap rate standardizes your analysis, letting you compare a downtown condo to a suburban duplex with total clarity.

Putting It to the Test: A Real-World Comparison

Let’s run through a quick, realistic scenario. You’ve narrowed your search down to three properties in your target market.

Property A: A Single-Family Home

- Price: $350,000

- Annual NOI: $19,250

- Calculation: $19,250 ÷ $350,000 = 0.055

- Cap Rate:5.5%

Property B: A Duplex

- Price: $480,000

- Annual NOI: $28,800

- Calculation: $28,800 ÷ $480,000 = 0.06

- Cap Rate:6.0%

Property C: A Small Apartment

- Price: $600,000

- Annual NOI: $33,000

- Calculation: $33,000 ÷ $600,000 = 0.055

- Cap Rate:5.5%

Just by looking at the cap rates, the duplex (Property B) immediately jumps out. It's not the cheapest or the priciest, but it generates the highest rate of return relative to its market value.

Interestingly, the single-family home and the small apartment have the exact same 5.5% cap rate. This tells you they are equally efficient from an income perspective, even though they operate at completely different price points. This simple comparison shows which property could work hardest for your investment dollar. It's a critical first pass in any serious real estate investment analysis.

How to Use Cap Rates to Screen Listings

Once you get comfortable with this, you can change how you look at properties. Instead of getting lost in the details of every single listing, you can use potential cap rates as a filter to sift through dozens of properties and zero in on real contenders.

By calculating a potential cap rate for properties you're considering, you can create a shortlist of homes that meet your minimum return threshold. This saves you countless hours by focusing your due diligence efforts only on the assets that have the strongest income potential from the start.

For example, you might decide you're only interested in properties with a potential cap rate of 6% or higher. Just like that, you've narrowed your search significantly. Now you can spend your valuable time digging deeper into the numbers and physical condition of properties that are already attractive on paper.

Common Pitfalls and Limitations of Cap Rate

While the cap rate is a fantastic tool for quickly sizing up a property, treating it as the only metric you need is a classic rookie mistake. Relying on it alone can be misleading.

Think of it as a single frame from a movie—it gives you a glimpse of the action but doesn’t tell you the whole story.

A cap rate is just a snapshot of a property’s performance over a single year, using current numbers. It’s a powerful starting point, but it completely ignores several critical factors that determine a property’s long-term success.

Understanding what the cap rate doesn't tell you is just as important as knowing what it does. Its simplicity is both its greatest strength and its biggest weakness.

What the Cap Rate Leaves Out

The cap rate calculation is backward-looking and static. It doesn't account for the future, which is where your actual profits (or losses) will happen. Here are a few massive blind spots you need to be aware of:

- Future Growth: The calculation doesn’t factor in potential rent increases or the property's appreciation in value over time. A home with a modest 5% cap rate in a rapidly growing neighborhood could be a far better long-term investment than one with an 8% cap rate in a stagnant area.

- The Power of Financing: Cap rate measures unleveraged return, meaning it assumes you're paying all cash. It completely ignores how a mortgage (leverage) affects your actual cash-on-cash return.

- Major Future Expenses: A seller’s stated income won't include big-ticket items looming on the horizon. A $15,000 roof replacement or a $10,000 HVAC system upgrade due in two years can instantly wipe out projected cash flow. This is why a home inspection is non-negotiable.

A cap rate is a measure of historical performance, not a guarantee of future returns. Always treat it as one piece of a much larger due diligence puzzle, not a shortcut to a final investment decision.

Avoiding Common Cap Rate Traps

The numbers a seller provides are often best-case scenarios. A savvy buyer knows to dig deeper and verify everything. Trusting provided rental figures without question is one of the quickest ways to overpay.

Always be skeptical of the income and expense figures you're given. A seller might conveniently omit vacancy costs or underestimate maintenance expenses to make the cap rate look more attractive. It's your job to create a realistic budget based on market averages and your own research, not on a listing sheet.

Ultimately, the cap rate is an excellent screening tool but a poor final decision-maker. Use it to quickly identify properties with good potential, but then your real work begins. Dive into the property’s condition, the local market trends, and get a thorough inspection before you ever make an offer.

Frequently Asked Questions About Cap Rates

Even after you get the hang of the formula, a few questions about cap rates always seem to pop up. Let's tackle the most common ones so you can feel confident when you're looking at your next home.

1. What's a typical cap rate for a residential property?

Cap rates vary widely by location. In high-demand urban areas, you might see cap rates of 3-5% because property values are high and appreciation is expected. In more affordable or slower-growing suburban or rural areas, cap rates might be higher, perhaps 6-8% or more, reflecting lower prices and potentially higher cash flow.

2. Is a higher cap rate always better when buying a home?

Not necessarily. For a home buyer, a very high cap rate could be a red flag. It might indicate the property is in a less desirable neighborhood, needs significant repairs, or has other issues that lower its market value. A lower cap rate often signals a more stable, desirable property in a prime location where long-term value appreciation is more likely.

3. How does my mortgage affect the cap rate?

It doesn't! This is a key point to remember. The cap rate calculation purposely ignores financing (your mortgage). It's designed to measure the property's income potential on its own, which allows for an apples-to-apples comparison between different properties, regardless of how a buyer plans to pay for it.

4. Why should I care about cap rate if I'm not an investor?

Thinking about cap rate helps you evaluate a home's long-term financial health. A property that could generate positive income if rented is a more secure asset. It gives you options for the future—if you ever need to move, you could potentially rent out the home instead of selling it. It's a good way to "stress-test" your purchase as a financial decision.

Tired of manually crunching numbers and second-guessing your analysis? Flip Smart takes the grunt work out of property evaluation. Get instant, accurate valuations, realistic renovation estimates, and clear profit projections for any property. Turn hours of tedious spreadsheet work into a few seconds of confident decision-making. Make your next investment your best one by visiting Flip Smart today.