It's an easy trap to fall into. You see a home's listing price, run some quick numbers on the mortgage, and think, "I can afford that." But the sticker price is just the beginning of the story.

The real cost of owning a home comes down to its carrying costs—the recurring, monthly expenses you pay just to keep the lights on and the title in your name. Think of it less like a one-time purchase and more like a monthly subscription for your home.

What Are Carrying Costs and Why Do They Matter?

Most new homebuyers focus on the down payment and purchase price. While those numbers are obviously critical, they don't tell you what it actually costs to live in the property month after month. The true measure of affordability isn't what you pay at closing, but what you can comfortably cover for the entire time you own the home.

This is exactly why nailing down your carrying costs is so important. These are all the expenses beyond your mortgage principal that relentlessly add up. Getting this right is the difference between enjoying your new home and becoming "house poor"—a nightmare scenario where your property expenses eat up so much of your budget that there's nothing left for savings, other goals, or your life.

The True Meaning of Affordability

Shifting your focus from the purchase price to the long-term carrying costs is a total game-changer for how you approach buying a home. It forces you to build a realistic, sustainable budget and ensures you don't get in over your head.

Understanding these costs upfront helps you in a few key ways:

- Prevent financial surprises: You’ll know the full monthly amount you need to cover, eliminating the shock of a budget that’s stretched too thin.

- Make smarter comparisons: You can accurately compare two homes by looking at their total holding costs, not just their list prices. I've seen cheaper homes with high HOA fees and taxes that were far less affordable than a slightly more expensive property with lower recurring expenses.

- Strengthen your negotiating position: When you have a crystal-clear picture of all associated costs, you can justify your offer price to sellers with real data.

A home's price tag is a one-time event, but its carrying costs are a long-term relationship. Mastering these numbers is the key to financial peace of mind as a homeowner.

Ultimately, calculating carrying costs gives you the confidence to know exactly what a home requires from you financially. It moves you from just buying a house to making a sound, data-driven decision that supports your goals for years to come.

What Really Goes Into Your Monthly Housing Bill?

When you’re mapping out your carrying costs, it's easy to fixate on the mortgage payment. But that's just one piece of the puzzle. Your actual monthly housing expense is a bundle of costs that lenders and real estate pros refer to by a simple acronym: PITI.

Getting a firm grip on PITI is the first real step to building a budget that won’t fall apart under pressure. Let’s break down what each letter stands for, so you know exactly where every dollar is headed.

Principal and Interest: The Heart of Your Mortgage

The biggest chunk of your monthly check to the lender is a mix of two things: principal and interest. They’re a team, but they have very different jobs.

- Principal: This is the money that actually pays down what you borrowed. Every dollar of principal chips away at your loan balance, building your home equity—the portion of the property you truly own. In the early years of a loan, the principal portion of your payment is frustratingly small, but it grows steadily over time.

- Interest: This is simply the fee your lender charges for loaning you the cash. It’s the cost of borrowing. For the first several years of most mortgages, the sad truth is that the vast majority of your payment goes straight to interest.

Think of it this way: principal is what you owe, while interest is what you pay for the privilege of owing it. With a standard fixed-rate mortgage, the combined P+I payment stays the same for the entire loan term, providing a predictable monthly cost.

Property Taxes: Your Stake in the Community

Property taxes are what you pay to your local government—the city, county, and school district—to fund essential public services like schools, roads, police, and fire departments. This is a non-negotiable cost of ownership.

Most of the time, your mortgage lender will collect a portion of your annual property tax bill with each monthly payment. They hold these funds in what's called an escrow account and then pay the government on your behalf when the bill is due. This system protects their investment (and yours) by ensuring the taxes are never missed. The amount you pay is based on your home's assessed value and local tax rates, both of which can and do change.

Homeowner's Insurance: Protecting Your Biggest Asset

If you have a mortgage, you’re required to have homeowner's insurance. No exceptions. This policy protects both you and the lender from financial ruin if something catastrophic happens, like a fire, a major storm, or theft.

Just like with property taxes, your lender will typically have you pay your insurance premium into your escrow account. They then handle the annual payment to the insurance company directly.

A crucial heads-up: standard insurance policies are notorious for what they don't cover. Disasters like floods and earthquakes almost always require separate, specialized coverage. It pays to shop around and really understand your policy, not just grab the cheapest option.

Beyond PITI: The Other Monthly Bills

While PITI forms the foundation, a few other common costs often get bundled into your monthly payment or are so consistent they might as well be. Ignoring them will wreck your budget.

- Private Mortgage Insurance (PMI): Put down less than 20% on your home? Your lender will almost certainly make you pay for PMI. This insurance doesn't protect you—it protects the lender if you stop making payments. It can add a hefty sum to your monthly bill until you build up enough equity.

- Homeowners Association (HOA) Fees: Buying a condo, a townhome, or a house in a planned community often comes with mandatory HOA fees. These monthly or annual dues pay for maintaining shared spaces and amenities, like pools, landscaping, security, and clubhouses.

These "extra" costs are just as real as your mortgage. It's also important to be aware of broader economic factors that can impact real estate. For example, rising inventory costs in the supply chain can signal future price hikes for building materials. The Logistics Managers' Index (LMI) hit a record high of 78.4 in May 2025, pointing to serious expansion partly due to stockpiling that led major retailers to warn of consumer price increases. You can find more data-driven insights on logistics trends at the-lmi.com.

Before we dive into the formulas, here is a quick summary of the core carrying costs every home buyer needs to account for.

Key Carrying Cost Components at a Glance

This table breaks down the most common carrying costs you'll encounter, how often you'll pay them, and a simple way to get an initial estimate.

| Cost Component | Payment Frequency | How to Estimate |

|---|---|---|

| Principal & Interest | Monthly | Use a mortgage calculator with current interest rates. |

| Property Taxes | Monthly (into escrow) | Check the local county assessor's website for tax rates and history. |

| Homeowner's Insurance | Monthly (into escrow) | Get quotes from multiple insurance providers (average is $100-300/month). |

| PMI | Monthly | Typically 0.5% to 2% of the loan amount annually, if applicable. |

| HOA Fees | Monthly or Annually | Review the property listing or ask the seller's agent for the exact amount. |

| Utilities | Monthly | Ask the current owner for average monthly bills for gas, electric, water, etc. |

Understanding these components individually is the key to building a comprehensive and realistic budget for your property.

Putting a Pencil to Your Monthly Carrying Costs

Knowing what goes into your monthly housing bill is one thing, but seeing how it all adds up for a real property is where the rubber meets the road. Let's move past the theory and calculate your actual, all-in monthly carrying costs. We can skip the complicated spreadsheets for now and use a simple, powerful formula to get a number you can act on.

The core equation you need to remember is: PITI + Utilities + HOA + PMI = Total Monthly Carrying Cost.

Let's walk through a real-world example. Imagine you're eyeing a property listed at $400,000, and you're planning to put down 10% ($40,000).

Breaking Down the Math Step by Step

We'll tackle each piece of this financial puzzle one by one. This process gives you a repeatable template you can apply to any home you are considering.

First, let's figure out the Principal and Interest (P&I). With a $360,000 loan amount (your purchase price minus the down payment) and a hypothetical 6.5% interest rate on a 30-year fixed mortgage, your monthly P&I payment would land around $2,275.

Next up are property taxes. This number varies wildly depending on your city and state, but a solid rule of thumb is to estimate about 1.25% of the home's value annually. For our $400,000 property, that comes out to $5,000 a year, or roughly $417 per month.

Homeowner's insurance is another critical piece. Your quote will depend on the home’s location, age, and construction type. A reasonable estimate for a home in this price range might be $1,800 per year, which is $150 per month.

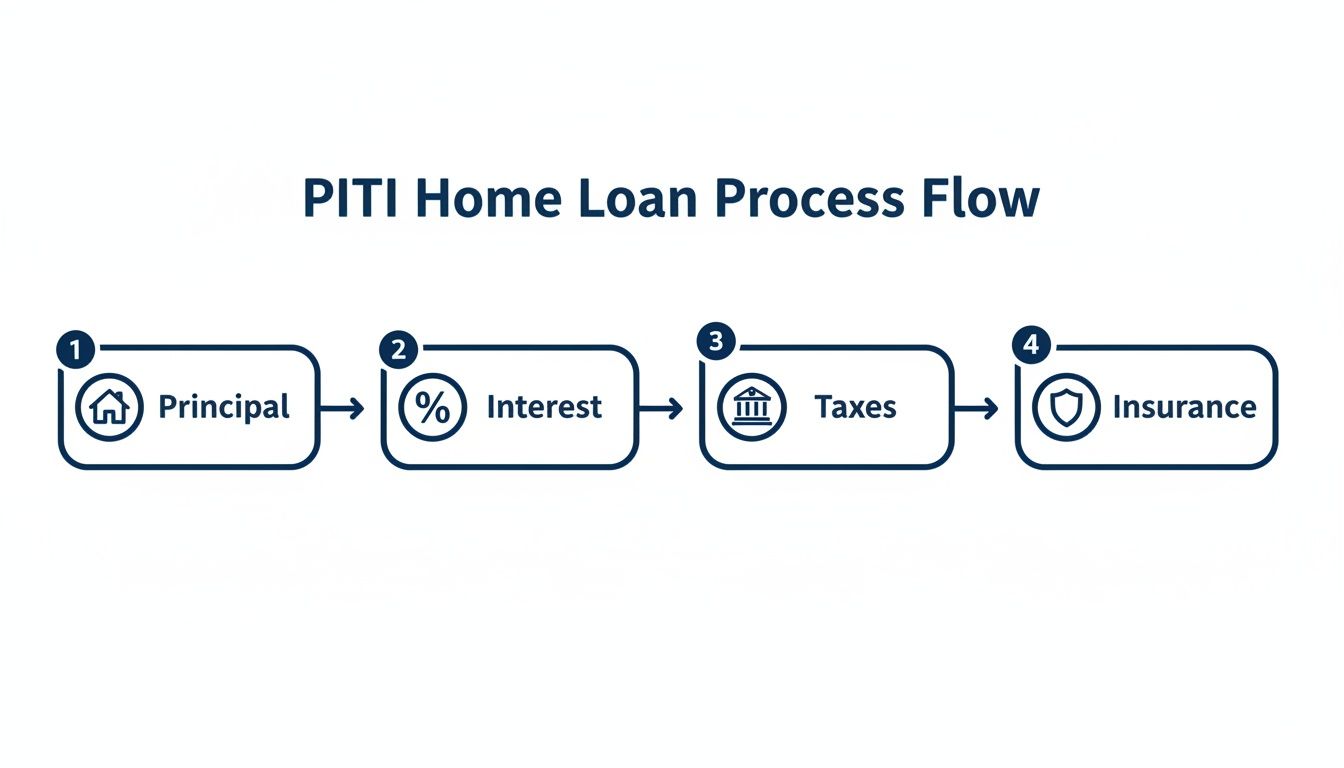

The image below breaks down these core PITI components—the foundation of every mortgage payment.

This visual is a great reminder that your single mortgage check is actually a bundle of four distinct costs: principal that builds your equity, interest for the bank, and escrowed funds for both taxes and insurance.

Adding the Other Essential Costs

Now we need to look beyond the basic PITI. Since our down payment is less than 20%, we have to factor in Private Mortgage Insurance (PMI). This typically runs between 0.5% and 1% of the loan amount annually. Let's use 0.75% of our $360,000 loan, which adds another $2,700 per year, or $225 per month.

Let's also assume this property is in a neighborhood with a Homeowners Association (HOA) that charges a modest $75 per month.

Finally, and this is a big one many people forget, we have utilities. For a mid-sized single-family home, a conservative guess for electricity, gas, water, sewer, and trash could easily be around $300 per month. Keep in mind, this can swing quite a bit based on your usage and the season.

Putting It All Together for a Final Number

Okay, let's add it all up to get the true monthly carrying cost for this $400,000 house:

- Principal & Interest: $2,275

- Property Taxes: $417

- Homeowner's Insurance: $150

- PMI: $225

- HOA Fees: $75

- Utilities: $300

Total Estimated Monthly Carrying Cost: $3,442

This final figure is the real number you need to budget for—not just the P&I payment the lender advertises. For investors, getting this projection right is absolutely fundamental. If you're looking at rental properties, understanding profitability metrics is just as crucial. A great resource on how to calculate cap rate on rental property can give you a much deeper insight into a deal's potential return.

Mastering these basic calculations is non-negotiable. For a deeper dive, check out our guide on must-know real estate math formulas to sharpen your analysis. This repeatable process will empower you to see past the flashy listing price and understand the true financial commitment of any property.

Beyond the Mortgage: The Real Costs of Owning a Home

Your predictable monthly mortgage payment (PITI) is a fantastic starting point, but it's only one piece of the puzzle. Getting truly ready for homeownership means bracing for the expenses that don’t show up on a loan estimate—the ones that can blindside new buyers and wreck a budget.

A solid rule of thumb many homeowners rely on is the "1% rule." It’s a simple but surprisingly effective guideline suggesting you should budget at least 1% of your home's purchase price every year for maintenance and repairs.

So, for that $400,000 property we've been talking about, you should be setting aside around $4,000 annually. That breaks down to about $333 a month, just for upkeep.

Budgeting for Routine Maintenance and Repairs

This maintenance fund isn’t for a disaster; it’s for the steady drumbeat of wear and tear that comes with any property. It’s for all the little (and not-so-little) fixes that inevitably pop up.

- Minor Headaches: Think leaky faucets, stubborn drains, or a garage door that decides to go on strike.

- Appliance Breakdowns: The dishwasher that suddenly won't drain or the fridge that stops cooling—usually at the worst possible time.

- Seasonal Chores: Cleaning gutters in the fall, servicing the furnace before winter hits, or power washing the deck come spring.

These tasks might seem minor on their own, but they add up fast. Having a dedicated savings account for them turns surprise bills into predictable, manageable expenses. For a more detailed look, our guide on estimating repair costs offers a deeper dive into what common home projects actually cost.

Planning for the Big Stuff: Capital Expenditures

Beyond the small fixes, your house has major systems with a limited shelf life. These are the big-ticket items known as capital expenditures (CapEx), and ignoring them is a recipe for financial stress. A new roof, an HVAC replacement, or a failed water heater can easily run into the thousands.

One of the smartest things a new homeowner can do is start a dedicated savings fund for these major replacements from day one. It's what ensures you're prepared when a $10,000 bill shows up five or ten years down the road.

Trust me, failing to plan for CapEx is a classic rookie mistake that often leads to high-interest debt when a critical system gives out unexpectedly.

Other Surprising Costs That Add Up

The surprises don't stop with repairs. To get a true 360-degree view of your budget, you have to account for a few other common expenses that are easy to forget in the excitement of buying.

- Landscaping and Yard Care: Whether you hire a service or buy and maintain your own equipment, keeping your lawn, trees, and garden beds in shape has a real cost.

- Pest Control: Depending on your location, regular treatments for termites, ants, or rodents might be a non-negotiable recurring expense.

- Property Tax Hikes: Your property taxes aren't set in stone. Municipalities can reassess your home's value—especially right after a sale—which can lead to a significantly higher tax bill than the previous owner paid.

By accounting for both routine maintenance and these other potential costs, you’re not just calculating carrying costs; you’re building a realistic financial roadmap that protects your investment and your sanity.

Smart Strategies to Lower Your Carrying Costs

Knowing your carrying costs is one thing; actively driving them down is where you start building real financial security. Small, smart decisions—made both before you buy and long after you get the keys—can make your home significantly more affordable.

Before you even think about making an offer, your most powerful lever is the down payment. Hitting that 20% down payment benchmark does more than just shrink your loan. It completely sidesteps the need for Private Mortgage Insurance (PMI), a costly add-on that can save you a bundle every single month.

And please, don't just take the first loan offer that comes your way. Shopping your mortgage can save you tens of thousands over the life of the loan. Even a fractional difference in the interest rate adds up to a massive long-term win. Apply the same logic to your homeowner's insurance—get multiple quotes to make sure you're getting solid coverage at a competitive price.

For a deeper dive, our guide on the cost of holding a property breaks down exactly how these initial choices ripple through your long-term expenses.

Proactive Steps After You Move In

Once the deal is closed, your focus needs to pivot to managing the ongoing operational costs. This is where active management really pays off, preventing minor issues from snowballing into budget-killers.

Challenge Your Property Taxes: Never assume your property tax assessment is non-negotiable. If you feel your home has been overvalued compared to similar properties nearby, you have every right to appeal the assessment. A successful appeal could lower your annual tax bill for years to come.

Embrace Energy Efficiency: Utility bills are a huge part of your carrying cost puzzle. Smart upgrades like sealing air leaks, beefing up insulation, or installing a programmable thermostat can seriously slash your monthly energy spend. For example, achieving smart thermostat energy savings is a relatively low-cost way to significantly cut down on heating and cooling expenses.

Prioritize Routine Maintenance: This is non-negotiable. Regular upkeep—cleaning gutters, servicing the HVAC system, checking for small leaks—is one of the most effective ways to head off expensive emergency repairs. A little prevention is worth a fortune in cure.

These strategies aren't just about pinching pennies; they're about taking firm control of your finances. Every dollar you shave off carrying costs is another dollar that goes toward building equity, saving for the future, or simply improving your quality of life.

This isn't just an issue for individual homeowners, either. The bigger economic picture shows that in 2024, U.S. inventory carrying costs ballooned to $302 billion. That's a staggering 13.2% annual jump, driven by supply chain chaos and higher interest rates. This macro trend underscores just how critical it is for homeowners to manage their own holding expenses with precision.

Frequently Asked Questions for Homebuyers

How much of my income should go toward carrying costs?

A great guideline for homebuyers is the 28/36 rule. It suggests your total housing costs (PITI) shouldn't exceed 28% of your gross monthly income. Additionally, your total debt payments—including housing, car loans, and credit cards—should stay below 36% of your gross income. Following this rule helps ensure you have enough money left over for savings and other life expenses.

Will my carrying costs change over time?

Yes, absolutely. While your principal and interest payment on a fixed-rate mortgage will stay the same, other costs will likely change. Property taxes can increase if your home's assessed value goes up, and homeowner's insurance premiums tend to rise over time. If you have an adjustable-rate mortgage (ARM), your interest rate and monthly payment could change significantly after the initial fixed period ends.

Can I ask the seller about their carrying costs?

You can and you should! A seller’s utility bills can give you a great baseline for what to expect, but take them with a grain of salt—your usage habits may be very different. You should also verify the property tax amount through public records rather than relying on the seller's number, as the assessed value can change after a sale. For HOA fees, always get the official documents to confirm the current dues and any upcoming special assessments.

Tired of juggling spreadsheets and guessing on your numbers? Flip Smart runs the math for you, calculating valuations, rehab costs, and holding expenses in seconds. Get the clarity you need to make smart, profitable decisions on your next deal. Analyze your first deal for free at flipsmrt.com.